FSO Safer: Risks to Yemen's neighbours (Part 1)

FSO Safer: Risks to Yemen's neighbours (Part 1)

Eritrea, Djibouti and Saudi Arabia's fishing industries face risks in case of an oil spill.

This is bigger than just Yemen

During the publicity campaign to raise funds for the salvage operation of the F.S.O. Safer, the US special envoy for Yemen Tim Lenderking relayed to Al-Monitor in July 2022 that he had been trying to emphasise to potential donors that this is an issue impacting not just Yemen.

“It's in their neighborhood,” said Lenderking. “We've also been emphasizing to any potential donor: This is not just the Yemen issue, or even just the Gulf issue. It's a global commerce issue.”

While we will get to the global commerce issue in a future post, there is the matter of potential negative reverberations on some of Yemen’s neighbours if the Safer spills its cargo.

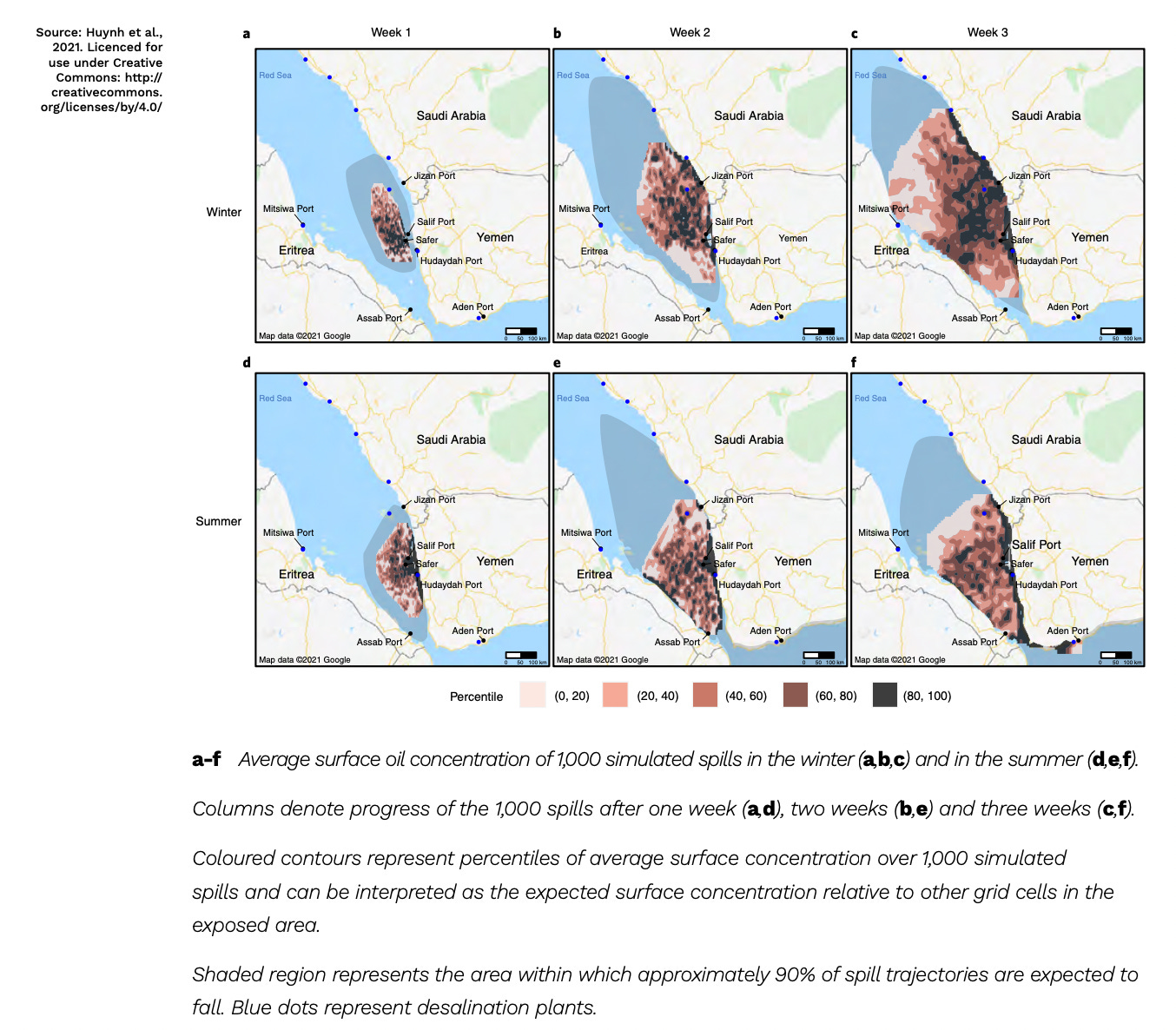

Looking at the scenarios modelled by Huynh et al in Nature and reproduced by Greenpeace, in a worst case scenario Saudi Arabia and Eritrea would be affected any time throughout the year (with oil hitting their coasts within three weeks), while Djibouti and even Somalia would be for some of the year (except for January to March). The spread could go as far as “300 km away with heavy to moderate amounts of oiling, and possibly some light oiling spreading to Aden 500 km to the south.”

Fishing industries at risk

The contamination of the Red Sea by an oil spill would lead to contamination of fish stocks, rendering them unfit for export or local consumption. While the fishing industries of Eritrea and Djibouti, both poor countries as it is, are relatively underdeveloped, there is potential for future growth. And Saudi Arabia, while relatively better developed, is still a net importer of fish and is investing hundreds of millions of dollars to expand its aquaculture industry.

(A brief description of each country’s fishing sector is contained below - mainly drawing from the UN’s Food and Agriculture Organisation (FAO).)

Eritrea

Eritrea produces only around 5,000 tonnes of fish per year (after peaking at just over 12,500 tonnes in 2000), almost exclusively captured in the Red Sea (particularly in the south). Annual per capita fish consumption is very low at 1.2 kg in 2017 (3.0 kg in 2000).

The most recent estimate from the FAO puts the total number working in the fishing industry at 3,600 people, mainly working in an ‘artisanal’ capacity and consisting of “foot fishers, canoe operators, traditional boats and trawlers”. (Industrial fishing predominating prior to 2007.)

Those fish with commercial value include those which are “either reef dwelling, such as groupers, snappers and emperors; demersal, such as lizardfish and breams; or pelagic, such as jacks, trevallies, mackerels, tunas, sharks, sardines and anchovies”.

Eritrea has two main harbours associated with fishing including Massawa in the north and Assab in south, as well as several in between (with some still under construction).

Fish is sold mainly within Eritrea as well as to Yemen.

Djibouti

Djibouti, located at the intersection of the Red Sea and the Gulf of Aden, produces only around 2,000 tonnes of fish per year mainly along the coast (with the north being the most productive), although it has potential for a lot more (4,500 tonnes commercial fish, 33,500 non-commercial fish) if more equipment and better distribution systems were in place. Annual per capita fish consumption is very low at 1.5 kg as of 2016.

The FAO puts its permanent fishing industry workforce at over 3,000 people, mainly working at a subsistence level in an ‘artisanal’ capacity.

Reef fish like grouper and snapper (as well as to a lesser extent barracuda) make up the demersal species, which represents 60% of total landed fish. Small pelagic fish such as sardines and anchovies are about 10-15%. Commercially important invertebrate species include cephalopods (e.g. cuttlefishes) and crustaceans such as penaeid shrimps, crabs and rock lobsters.

Djibouti’s two main fish sites are Tadjoura in the Gulf of Tadjoura and the Arta region in the south-east. And to the east of the Arta region sits the capital Djibouti city, which also has a fishing port used for offloading, processing, storage and distribution.

Fish is sold mainly within Djibouti, while exports only amount to about 500 tonnes a year mainly to Gulf States and the European Union.

Saudi Arabia

Saudi Arabia, which borders both the Red Sea in the west and the Arabian Gulf in the east, produced around 160,000 tonnes of fish per year in 2020 (60,000 captured and the remaining 100,000 from aquaculture production). Yet it imported 215,000 tons of seafood such as tuna, sardines and Basa, and exported only 60,000 tons. Annual per capita fish consumption was 13.5 kg as of 2013.

Despite the Red Sea’s much greater size compared to the Arabian Gulf, it only produced half the captured quantity of fish.

Fishing out in the sea is conducted by a mix of artisanal fishermen and industrial operations. (In 2018, there were 8,653 small boats and 158 large industrial fishing boats in Saudi Arabia.) Shrimp are the main catch of the latter, while fish species such as Spanish Mackerel, Groupers, Snappers and Barracudas) are caught by the smaller operators.

There are over 30,000 fishermen employed in Saudi Arabia, the vast majority foreign workers.

Under its Vision 2030 plan, Saudi Arabia plans to produce 600,000 tons per year and generate up to 200,000 jobs working directly and indirectly in the fishing industry. Half of these jobs would go to locals. (Foreign workers make up over 70% of the private sector in Saudi Arabia.) The main vehicle for this ambitious growth is the National Aquaculture Group or Naqua, the Middle East’s largest fishing industry firm, based near Jedda’s port halfway up the Kingdom’s west coast on the Red Sea. It is a “large-scale farm working up and down the fisheries value chain — from on-site feed production, to selling products through various firms”. Producing shrimp, Barramundi fish, and sea cucumber, it made up 86% of total Saudi aquaculture production in 2018. It has a rival though - Tabuk Fish - which signed a deal last year with the futuristic NEOM city further north up the Red Sea to establish the largest fish farm in the whole of the Middle East and Africa. While these cities and ports are too far away to be directly touched by an oil spill, the disruption to shipping in the Red Sea region will hinder the timely exports of fish the Kingdom is heavily investing in.

In Part Two, we will look at the potential impact which an oil spill could have on the region’s water supplies, tourism and imports of vital food, fuel, aid, medicines.